Home Buying Process in a Nutshell

Home buying can be overwhelming. Let’s demystify it.

Before you start browsing listings, it's crucial to understand your financial situation. Calculate your monthly income, expenses, and how much you can comfortably afford to spend on a home. Don't forget to account for additional costs like property taxes, insurance, and maintenance.

A good real estate agent can be invaluable. They know the market, can help you find properties that meet your criteria, and guide you through the negotiation process. Plus, they can provide insights that you might not have considered.

There are different types of loan. Some general guidelines are described below.

Conventional loan: The most common type of home loan. Down payment can be between 3-20% with a term of 15-30 years. May require mortgage insurance if down payment is under 20%. Minimum credit score required is around 620.

FHA Loan: Loans designed for those with high debt-to-income ratios and low credit scores. Most commonly issued to first-time homebuyers. Down payment can be between 3.5 -20% with a term of 15-30 years. Mortgage insurance is required for 11 years or life of the loan. Minimum credit score required is around 500.

VA Loan: For veterans. No down payment is required. Minimum credit score required is around 640.

USDA Loan. Usually for properties in eligible rural areas as defined by the USDA. Minimum credit score required is around 640.

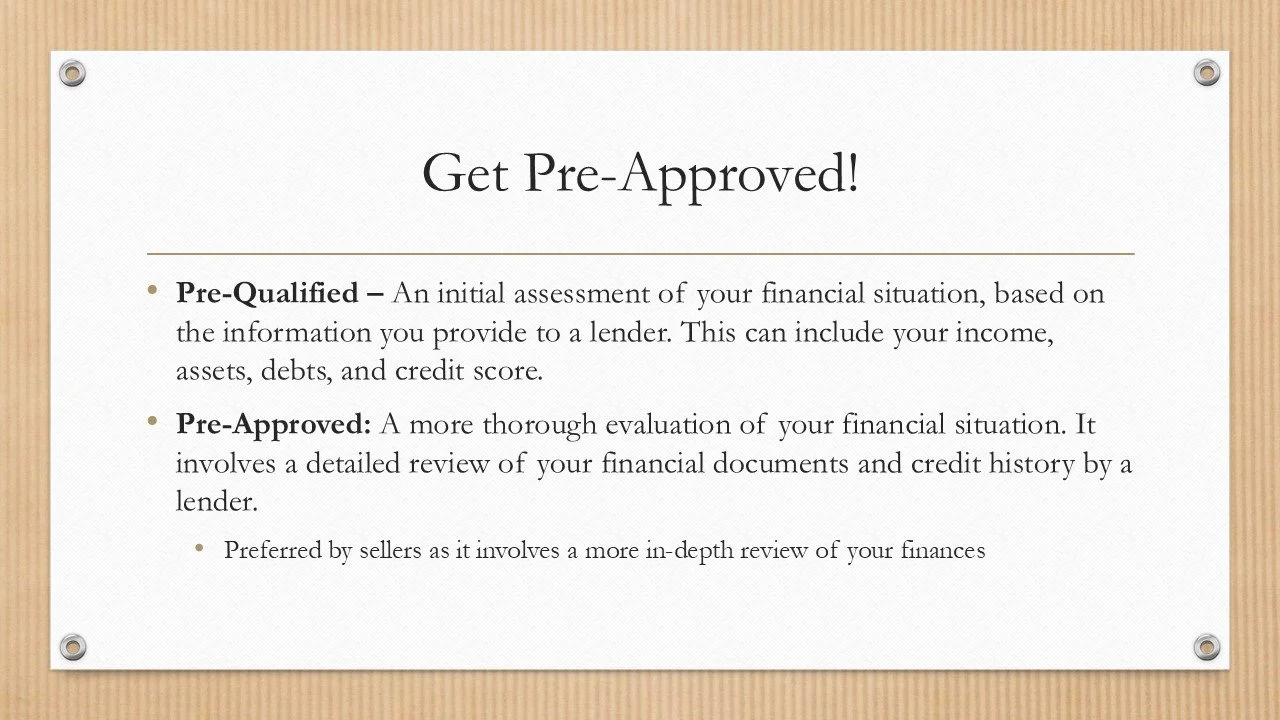

Getting pre-approved for a mortgage gives you a clear idea of how much you can borrow and shows sellers that you're a serious buyer. It involves a lender reviewing your financial information and providing you with a letter stating the amount you're approved for.

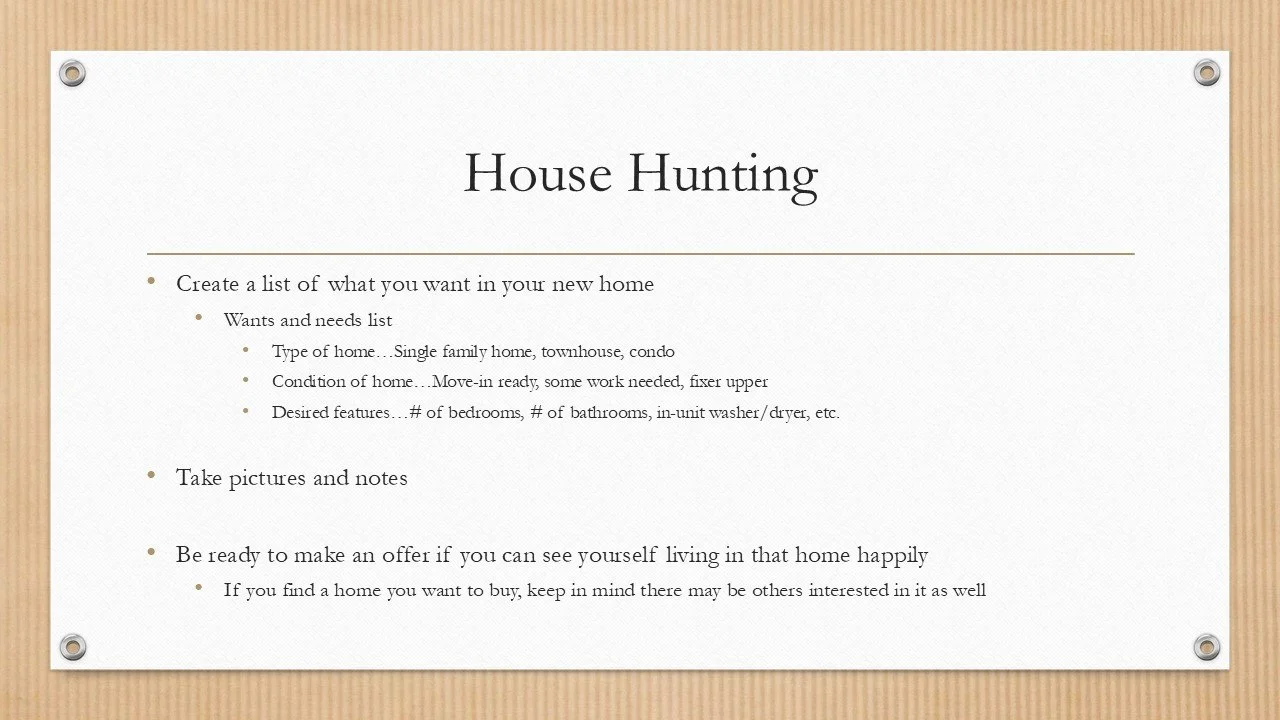

Location is key. Research different neighborhoods to find one that suits your lifestyle and needs. Consider factors like commute times, school districts, amenities, and future development plans.

Seeing a home in person can give you a much better feel for the space than pictures online. Attend open houses and schedule tours for properties you're interested in. Don't be afraid to ask questions about the home's history, maintenance, and any potential issues.

While it's important to have your must-haves, be prepared to compromise on some features. Finding the perfect home might take time, and you might need to adjust your expectations based on what’s available in your price range.

Handling Disappointment When Your Offer Isn’t Accepted

In the journey of finding your perfect home, it’s easy to become emotionally attached to a property that seems to tick all the boxes. However, it’s important to manage your expectations and emotions, especially if your offer isn’t accepted by the seller. Here’s how to stay positive and keep moving forward:

1. Understand the Market Dynamics

Real estate is a competitive market, and multiple factors can influence a seller’s decision. The seller might have received a higher offer, or they might have different terms in mind. Remember, it’s not a reflection of your worth as a buyer but a part of the process.

2. Keep Emotions in Check

It’s natural to feel disappointed when an offer isn’t accepted, but try not to let it deter you. Staying emotionally balanced helps you remain objective and ready to explore other opportunities. Treat each offer as a step forward, regardless of the outcome.

3. Stay Flexible and Open-Minded

Be open to the possibility that there might be an even better property waiting for you. Flexibility in your preferences and criteria can open up new opportunities that you might have overlooked initially.

4. Learn from the Experience

Each rejected offer is a learning opportunity. Discuss with your real estate agent why the offer might not have been accepted and what adjustments can be made for future offers. This can strengthen your strategy and increase your chances of success.

5. Focus on Your Long-Term Goals

Remember your long-term goals and the reason you’re buying a property. Keeping the bigger picture in mind can help you stay motivated and resilient throughout the process.

6. Trust Your Agent

Your real estate agent is there to guide and support you. Trust their expertise and advice. They have the experience to navigate these ups and downs and can help you find a property that meets your needs.

7. Practice Patience

Finding the right property can take time. Practice patience and give yourself grace. The right home is out there, and with persistence, you’ll find it.

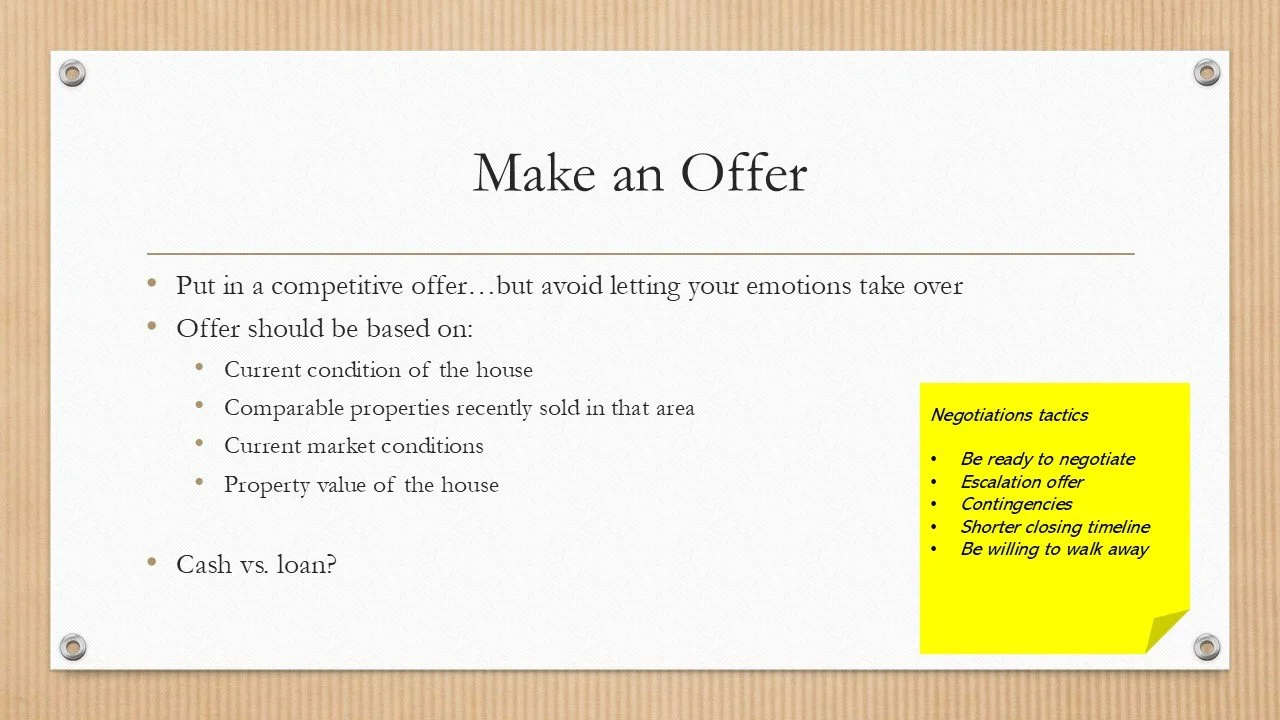

1. Sign the Purchase Agreement

Once the offer is accepted, both the buyer and seller will sign a purchase agreement. This legally binding document outlines the terms and conditions of the sale, including the purchase price, closing date, and any contingencies.

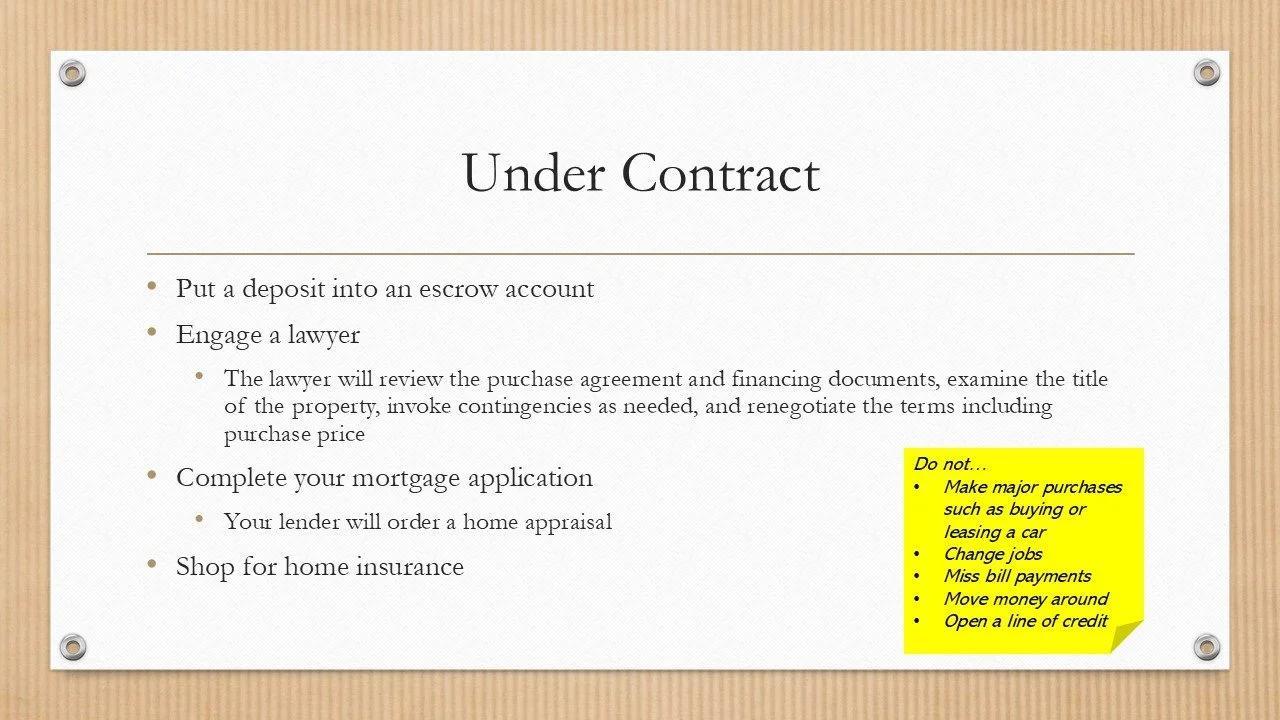

2. Deposit Earnest Money

You, as the buyer, will deposit earnest money, usually 1-2% of the purchase price, into an escrow account. This shows the seller that you are serious about the purchase. The earnest money is typically applied towards the down payment or closing costs.

3. Engage a lawyer

Here’s what to expect from your lawyer during this phase:

1. Review the Purchase Agreement

Your lawyer will carefully review the purchase agreement to ensure that all terms and conditions are favorable and legally binding. They will look for any potential issues or ambiguities and negotiate any necessary changes with the seller’s lawyer.

2. Title Search and Clearance

One of the primary responsibilities of your lawyer is to conduct a thorough title search. This involves examining public records to verify the property's ownership and ensure there are no outstanding liens, claims, or encumbrances that could affect the transfer of ownership. If any issues are discovered, your lawyer will work to resolve them.

3. Coordination with Lender

Your lawyer will coordinate with your lender to ensure all financing documents are in order. They will review the mortgage agreement to ensure that the terms are clear and protect your interests.

4. Handling Legal Documents

Real estate transactions involve a plethora of legal documents. Your lawyer will prepare, review, and ensure the proper execution of all necessary paperwork, including deeds, affidavits, and closing disclosures.

5. Managing Contingencies

The purchase agreement may include contingencies such as financing, inspections, and appraisals. Your lawyer will ensure that all contingencies are met within the specified timelines and address any issues that arise.

6. Negotiating Repairs or Credits

If inspections reveal any issues with the property, your lawyer will negotiate with the seller’s lawyer for repairs or credits. They will ensure that any agreements made are documented and enforceable.

7. Explaining Closing Costs

Your lawyer will review the closing disclosure and explain all associated costs, ensuring there are no surprises at closing. They will make sure that all fees are accurate and fair.

4. Secure Financing

Work with your lender to finalize the mortgage. This includes submitting necessary documents, undergoing a credit check, and ensuring the lender's requirements are met. The lender will also order an appraisal to verify the property's value.

5. Shop for home insurance

Provide proof of insurance to your lender. This usually involves sending a copy of the insurance binder or certificate of insurance, which outlines the coverage details.

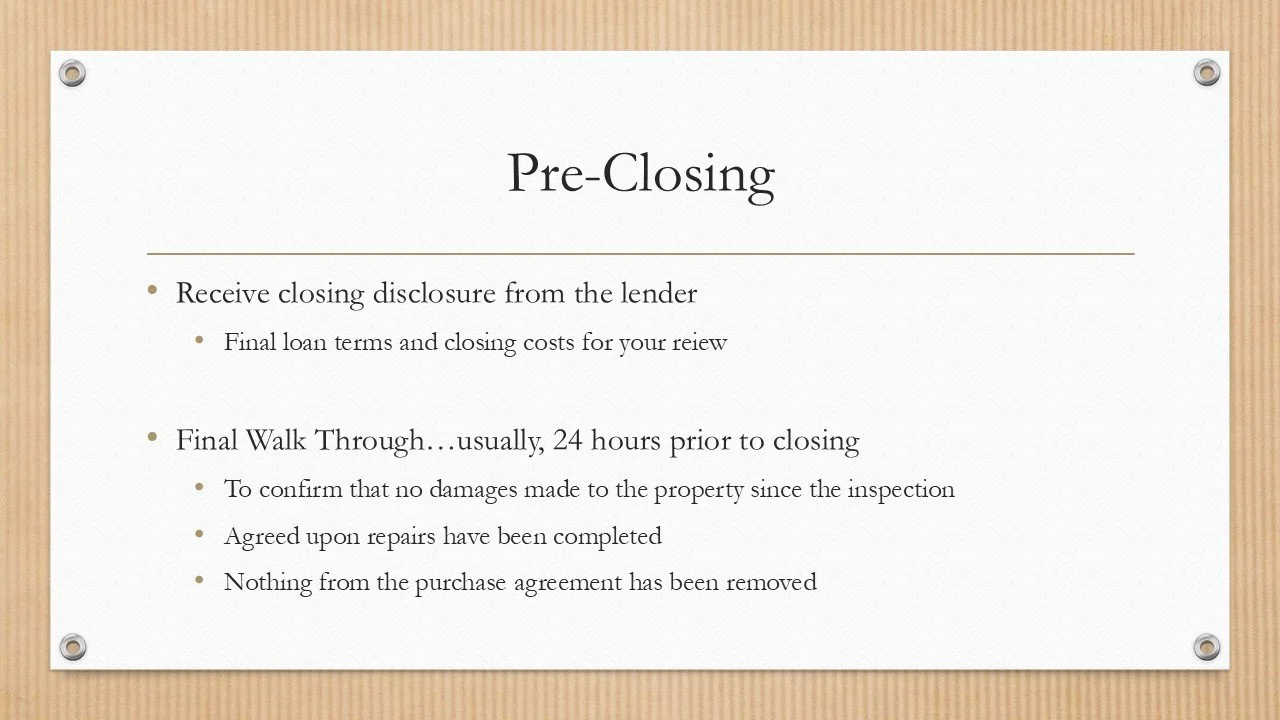

1. Closing Disclosure from the Lender

Receive the Closing Disclosure: Your lender will provide a Closing Disclosure at least three business days before closing. This document outlines the final loan terms, including the loan amount, interest rate, monthly payments, and closing costs.

Review Carefully: Compare the Closing Disclosure with the Loan Estimate you received when you applied for the mortgage. Ensure that the terms match and that there are no unexpected changes.

Ask Questions: If you have any questions or notice discrepancies, reach out to your lender immediately for clarification.

2. Conduct a Final Walkthrough

Schedule the Walkthrough: Typically, the final walkthrough is scheduled within 24 hours before closing. This is your last chance to inspect the property before you take ownership.

Check Repairs: Verify that any agreed-upon repairs have been completed to your satisfaction.

Inspect the Condition: Ensure that the property is in the same condition as when you made the offer. Look for any new issues that might have arisen.

Test Systems and Appliances: Check that all systems (e.g., HVAC, plumbing, electrical) and appliances are functioning properly.

Gather Documents: Bring necessary identification, proof of insurance, and any required funds in the form specified by your lender (e.g., cashier's check).

Review Final Numbers: Double-check the final figures on the Closing Disclosure to ensure you’re prepared for the exact amount due at closing.

Sign Documents: During the closing meeting, you will sign all required documents, including the mortgage agreement and deed.

Pay Closing Costs: You will also pay any remaining closing costs as outlined in the Closing Disclosure.

Receive the Keys: Once all documents are signed and funds are disbursed, you'll receive the keys to your new home.

For those of you who have purchased a property, what was your experience like? What advise would you give to first-time homebuyers?

For first-time homebuyers, which part of the process appears to be complex or overwhelming?